- Frazis Capital Partners

- Posts

- May 2026 Investment Update

Dear investors and well-wishers,

We started April with one of our highest cash balances and finished up 25%, which put us at +70% over the last twelve months and lifted our three year return to 34% pa, over quite a challenging period.

The month surprised us, as we were positioned so defensively at the start. But when the signals came we bought aggressively and got set before a wave of quant buying. We knew the buying was coming, but we didn’t expect it so soon. Some targets reversed quickly and were closed for small losses. Others have already hit 2x, 3x and higher profit targets.

Computers can be quite good at this, as others discovered long before us.

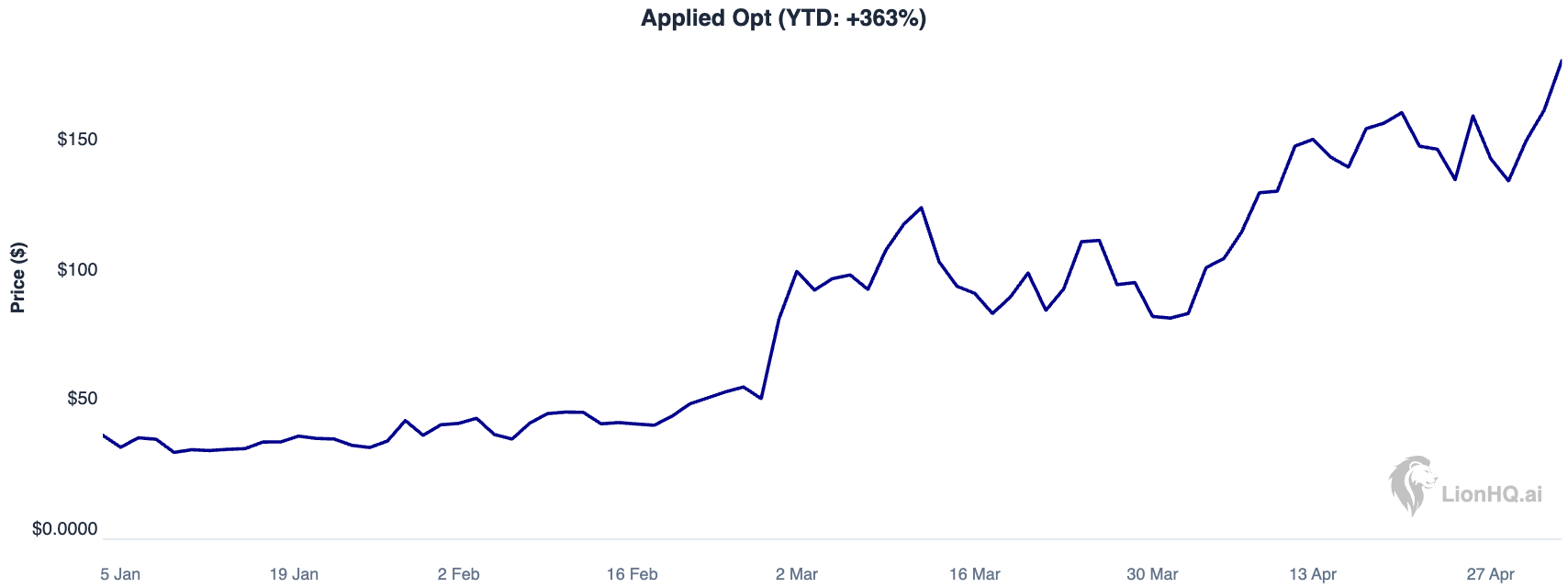

The CPU thesis we discussed in our last letter came to fruition, with a >100% realised move in AMD. Our semiconductor exposure was weighted heavily towards mega caps like Nvidia and Broadcom, but we had small positions in ‘bottleneck’ companies. AAOI is up ~6x from our purchase, but we closed entirely when it hit its final profit target, for an total return of 3.6x, towards the higher end of our typical 3.5-4x profit target.

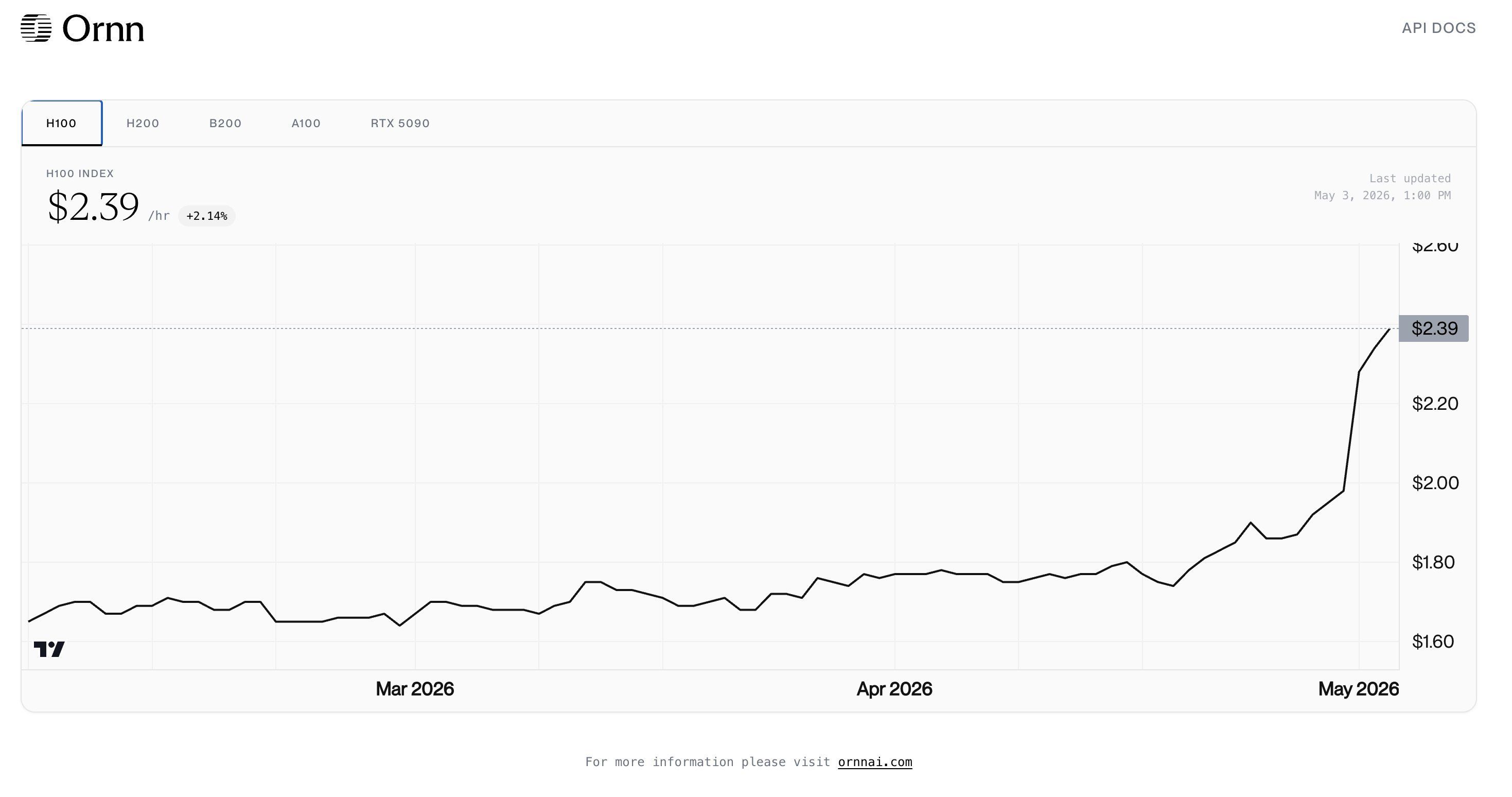

GPU rental pricing trends have been strong - this is a key driver of neocloud revenues, so expect these companies to rise and fall in line. At the moment, demand is exceedingly strong.

We’ve been through enough of these moments to know how important it is to harvest profits in these kinds of markets, knowing that we will likely get another re-entry point in the near to mid term.

This is one of those periods where the vast majority of stocks are underperforming, so you have to find your way into the 10-20% of stocks that are doing well. The reason so many active managers are struggling is because there’s such a narrow path to success this year, and quant firms like Jane Street are systematically harvesting tens of billions of dollars from the market, which all comes out of the active pool.

This is the third time we’ve been in a defensive high cash position and caught a wave of buy signals. The last two times (November 2023 and a similar time last year) the market (and our fund) rallied for about six months, though the major move was in the early stages when the systematic quant selling flipped to buying.

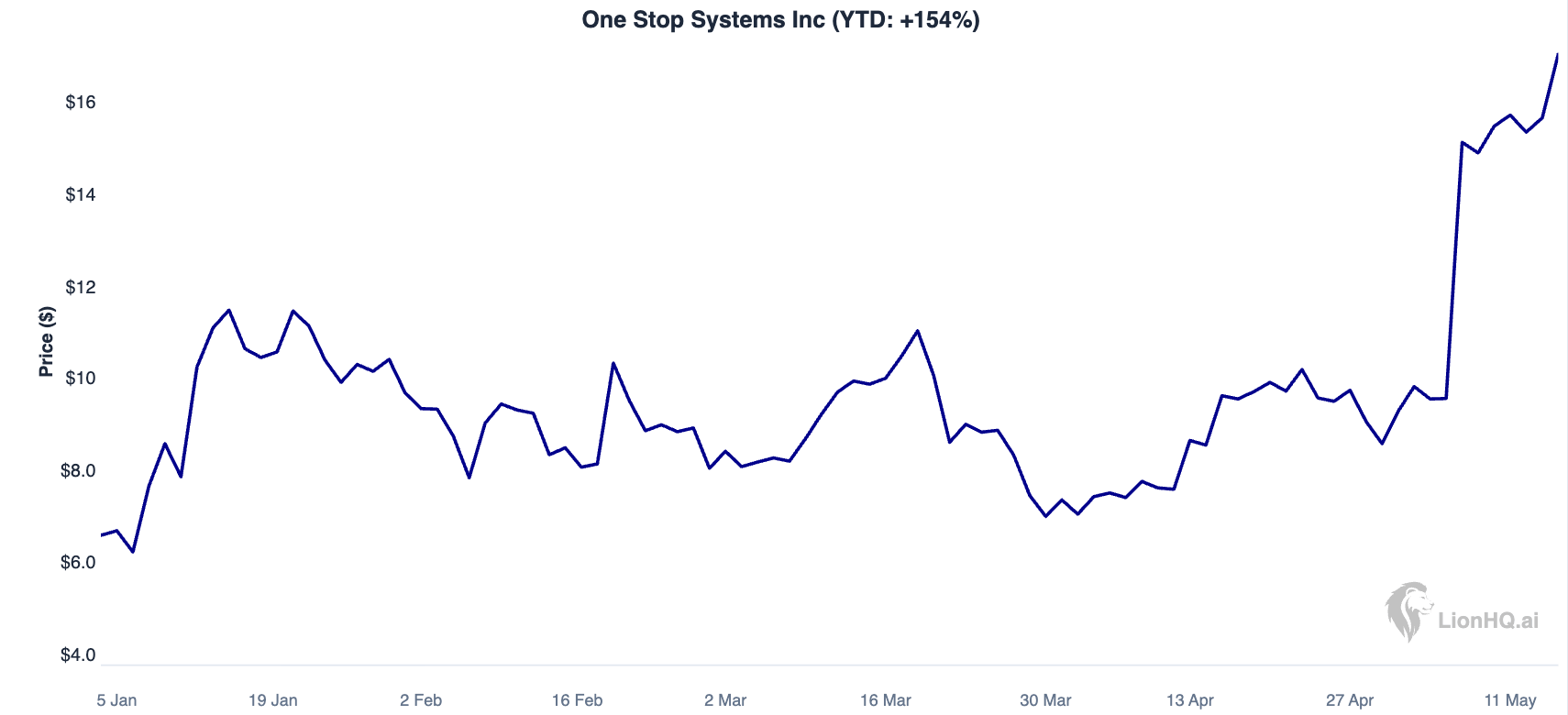

OSS

We’re heavily weighted to large and megacap stocks, but to give an example of a small cap purchase, we bought One Stop Systems (OSS) based in California, that designs rugged, enterprise-class compute for AI at the "edge," specializing in the most challenging environments in defence and industry. These applications require local AI inference, and specialized equipment housing the required hardware.

OSS supplies boxes of compute to P-8 Poseidon submarine-hunting aircraft, autonomous mining trucks, and defence drones, all with local AI inference requirements and hot, hostile, vibrating operating environments. Not situations where you want to be relying on access to the cloud.

The company has net cash and announced significant recent orders which we expect to continue.

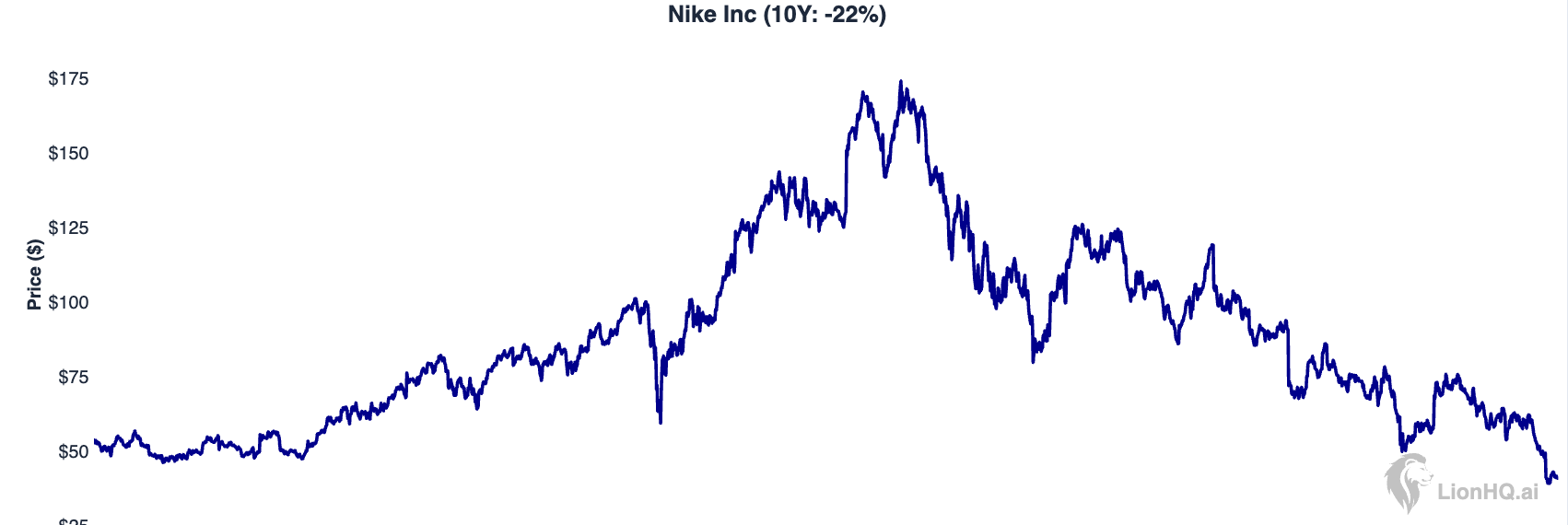

It’s been particularly brutal for those investing in compounders, obviously in SaaS, but also across the consumer space. Once consumer favour turns negative in companies like Nike, it’s difficult to turn it around.

Outlook

The CTAs and momentum strategies were heavy buyers in April, shortly after us as it turned out. The next set of systematic buying will come from the slower moving volatility targeters, but the bulk of this will likely land this month, so the easy part of the move is probably over.

We went fairly broad in our buys, picking up a number of beaten down midcaps as well as the obvious winners in semiconductors. While we did crystalize some small losses, you don’t need a quant model to see that the SaaS sell-off has stabilized.

For the sell-off to continue the AI bear case will need to show up in company results, and so far revenue growth has actually accelerated for some companies. So the path to success in the latter half of the year may be in the same companies that were punished so severely over the last six months.

Fortunately with our process we don’t need to guess, and can go for those 2-3x returns from the lows knowing that if we’re wrong, we’ll be out of the positions quickly with manageable losses. There’s no need for risky concentrated, high conviction swings in this market.

We’re still heavily invested but have been net sellers recently, partly as some positions hit 2-3x targets, and partly from closing buys that didn’t work.

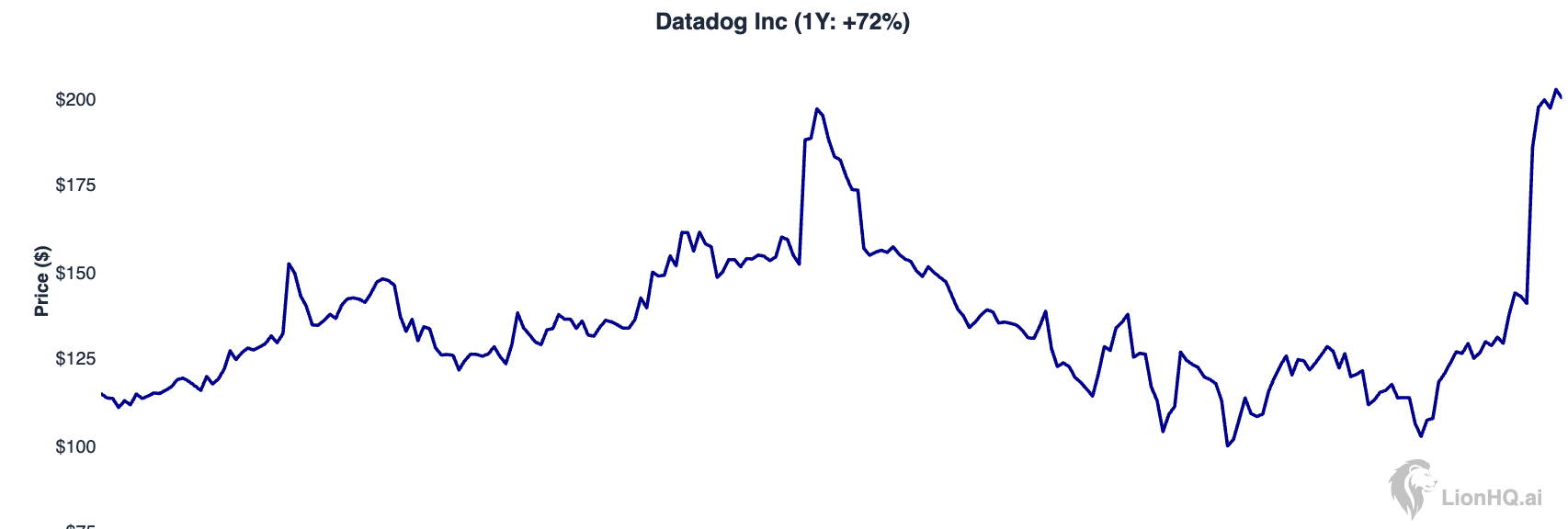

The major open question is whether beaten down companies that reaccelerate start performing again, or the bleed-out continues. So far there have been early signs of change, with companies like Datadog, erstwhile in the AI-loser category, rapidly recovering their drawdowns after a strong report.

This is our current research focus, particularly now that SaaS destruction moved from fringe to consensus. So following the principle that the market moves in the direction of maximum pain, the next major move may well be up.

Best

Michael